Since the first one was launched in 1994, target-date mutual funds have increasingly gained in popularity among investors. Over the last decade, target-date funds have become a staple of 401k other retirement investment plans. With that being said, total assets invested in such funds have soared from $111.9 billion in 2006 to $644 billion in 2014.

Q: What exactly are target-date funds?

A: These are funds with a specific target retirement date – corresponding to an investor’s estimated retirement year – that are comprised of cash, stocks, and bonds. Over time, the funds, which normally invest in a number of other, underlying funds managed by the parent company, gradually transition to a more conservative asset allocation as the target retirement date approaches. Individuals using these investments are freed from the burden of reallocating their assets as they age and are spared the duty of searching for suitable funds in various categories to build a well-diversified portfolio. While many companies offer funds of varying retirement years, these providers differentiate their offerings through unique allocation criteria. Currently, T. Rowe Price, Fidelity Investments, and Vanguard are the largest players in this space. With that being said, investors should be aware that these funds are not always the best choice for all investors.

The Good

The biggest advantage target-date funds enjoy is their simplicity. It is this characteristic that makes them appealing to individuals who do not have much investing experience. This “set it and forget it” mentality has caused the popularity of target-date funds to increase substantially, particularly within participant-directed 401k plans. Outside of retirement accounts, these funds could be appealing for individuals with smaller investment portfolios, such as those just beginning to save for retirement, as achieving proper diversification is more difficult with smaller account balances. In these cases, target-date funds offer a simple solution and allow such individuals to gain exposure to a myriad of underlying funds, achieving broad diversification with much lower capital. Aside from these situations, investors with more money to invest should keep in mind a few additional considerations before getting on the target-date fund bandwagon.

The Bad

While target-date funds do offer some advantages, they also pose a few challenges and risks that are unknown to some investors. First, target-date funds do not offer the same amount of flexibility as a custom portfolio because they follow one investment philosophy – that of the parent company. In addition, the target date funds are only comprised of underlying funds of that issuing company, thereby inhibiting the ability to pick investments from different companies. For instance, while one fund provider may have a strong lineup of U.S. equity funds to draw upon, it may not have the same expertise and research capabilities in the fixed income or emerging market universes.

Further, target-date funds falsely assume that all individuals retiring in a given year have the same personal financial circumstances and risk tolerances. For example, an individual that has steady sources of post-retirement income – such as a pension, rental property income, or part-time work – may be able to tolerate higher risk in his/her investment portfolio than an investor who will look to source the majority of his/her retirement income from the investment portfolio. Target-date funds do not take these details into consideration. Moreover, target-date funds are less flexible in terms of tax-planning. Since these are designed to be the sole investment in a portfolio, it is not possible to harvest investment losses in underperforming asset classes to offset realized capital gains, a practice that has been shown to improve investment results over time.

Finally, the most alluring quality of these funds, their simplicity, could ultimately be their largest downfall. Research suggests that this simplicity gives some investors a false sense of security and leads them to believe that they will be ready for retirement just by using a target-date fund. For example, a 2012 study sponsored by the Securities and Exchange Commission (SEC) found that only 36% of respondents knew that target-date funds do not provide guaranteed retirement income. Furthermore, another 30% of individuals who owned target-date funds reported that they did not know the correct definition of “target date” in the name of the fund. Another mistake some investors make when utilizing these funds is combining target date funds with additional stock or bond funds, which can change the overall portfolio asset allocation and give the portfolio a different risk profile than what was desired.

Comparing Different Companies

While there are many target-date funds geared toward the same chosen year, they are far from the same in their investment approach. When investing in these types of funds, it is important to consider the glide-path taken by its managers. Broadly, a glide-path refers to the formula used by a particular company to adjust the mix of stocks, bonds, and cash in the portfolio in relation to the target date. Since different companies follow different glide-paths, their returns can vary significantly from year-to-year.

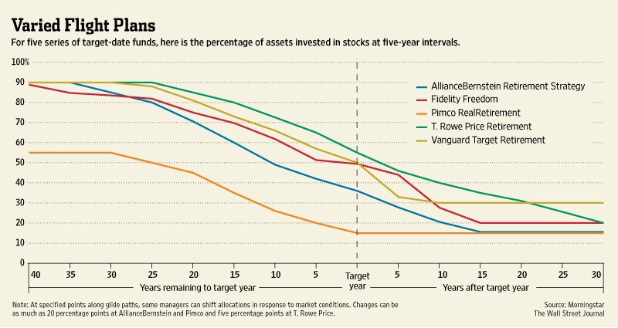

As seen in Figure 1, while Fidelity and Vanguard allocate 50% of assets to equities at the target date, PIMCO invests just 15% of the fund’s assets in stocks at retirement. This divergence in allocation can significantly affect returns, as evidenced in 2013 when target-date funds with larger allocations to equities significantly outperform those with heftier bond sleeves. Before investing, it is critical to consider the glide-path of a fund in comparison with your overall risk tolerance and income needs.

Figure 1: Looking Toward the Future

Considering the strong rally the domestic stock market has enjoyed over the last few years and the fact that interest rates remain near historical lows, the current investment environment could prove particularly challenging for target date funds given their lack of flexibility. Since target-date funds generally use the historical returns of various asset classes to determine their glide-path, these funds may have a harder time adapting to the market environment going forward, as we believe fixed income returns are likely to be lower than their historical average.

At Condor Capital we believe that a customized, flexible investment approach is the best option for most investors seeking to build their retirement nest egg. For instance, over the last few years, we have maintained an underweight allocation to non-U.S. equities in our clients’ portfolios to reflect our higher optimism regarding the domestic economy versus the economies of other major nations. Additionally, we have taken several steps to reduce the interest rate risk within clients’ fixed income sleeve. As the interest rate environment normalizes in the future and rates drift higher, we may then look to rebalance towards a more-normal allocation. Investors in funds with predetermined glide paths cannot take advantage of strategic shifts such as this. In all, “set it and forget it” investment options do not take into account the current market dynamics or an investor’s particular circumstances. While target-date funds accomplish a few key goals and may be right for certain investors, they lack in the flexibility and caution that is needed to get the most out of your money as you approach retirement.