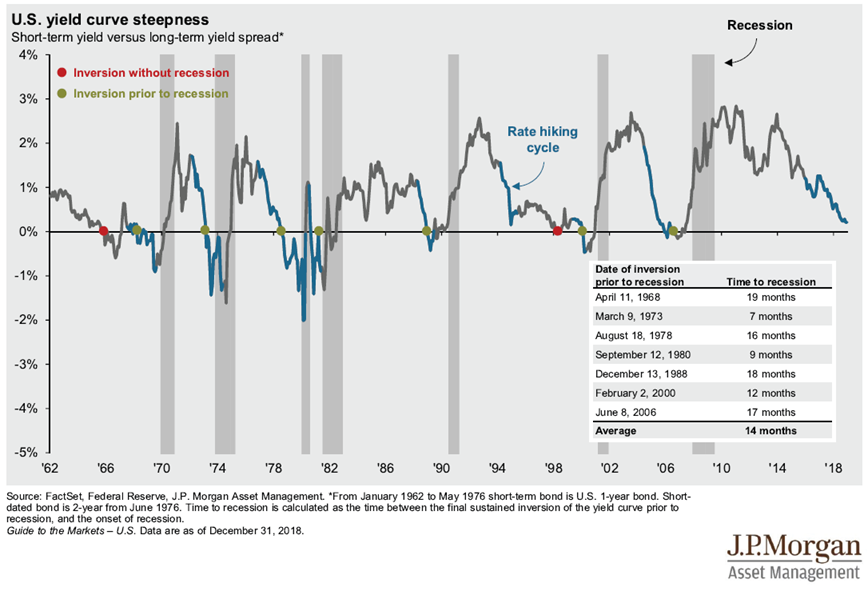

Much noise has been made about the U.S. yield curve’s inversion with 3-month Treasury yields trading roughly around the same price as 10-year Treasuries. Pundits have been quick to declare that a recession is imminent, citing similar situations where the yield curve has inverted before recessions in the last 60 years. While it is true that the yield curve has inverted before past recessions, it must also be noted that there were moments of inversion that were not followed by a recession over the last 60 years as well. There is also no accurate way of timing when a recession might occur even after a yield curve inversion. The chart below highlights this:

As you can see from this chart, there have been multiple times that a yield curve inversion has not led to a recession. Additionally, when recessions do follow, there is great variance in the amount of time between inversion and recession. The average lag of 14 months shows that this is far from a clear and direct pattern.

Prudent investors would also be wise to realize that while the short end of the yield curve might be the flattest it has been since 2007, the long end of the curve is still sloping upwards, suggesting that the inversion is more influenced by international capital flows than domestic concerns for a significant economic slowdown. It is of note that underlying economic data is still positive and none of the typical metrics associated with a recession, such as high unemployment numbers and rising debt service ratios, are present.

On Monday, March 25, 2019, 10-year German bund yields were trading at a negative yield of -0.003%. Bund yields, which serve as a proxy for risk-free interest rates in the Eurozone, declined in the wake of less than stellar German manufacturing data. The export-dependent German market has been adversely affected by slowing demand in China, their largest trading partner. Furthermore, the ongoing Brexit negotiations and the lack of a clear resolution creates uncertainty that investors have been keen to avoid. Negative yields in such a sizeable market – BIS data suggests the total German bond market to be valued at just over 3.6 trillion euros as of March 5th – inevitably push investors to search for higher returns in other markets.

Bank of America Merrill Lynch estimated Friday an additional $12.1B has made its way to fixed income portfolios in the past week, and with negative yields in Germany and Japan, it is safe to assume that much of this cash made its way to U.S. Treasuries. This surge in demand from European bondholders to the U.S. has pushed prices higher and, in turn, yields lower over the past three months, driving 10-year Treasury yields from a late December level of 2.8% to Monday’s 18-month low of 2.449%.

While the relationship between yield curve inversion and recession is not nearly as direct as some alarmist pundits may be indicating and timing a recession is close to impossible, there are still some important points to be gleaned from this development. First, international markets are slowing down, especially when compared to their American counterparts. Here at Condor we have remained underweight in international equites for some time now compared to our peers because we remain skeptical of international corporations’ ability to post attractive returns when compared to U.S.-based firms. More importantly, this inversion should further affirm the need for investors to maintain well-diversified portfolios that adhere to their investment goals. Rather than attempting to time inverse yield curves and market movements, investors are always best suited by having diversified exposure to a large variety of asset classes to better insulate themselves from rare but unpredictable market movements.